NVIDIA N1X ARM Laptop Chip: 20 CPU Cores, RTX 5070-Class GPU, and 8 Dell/Lenovo Models Launching Spring 2026

March 26, 2026

Mistral Small 4 Review: How the 119B MoE Open-Source Model Matches GPT-OSS 120B at 40% Lower Latency

March 27, 2026

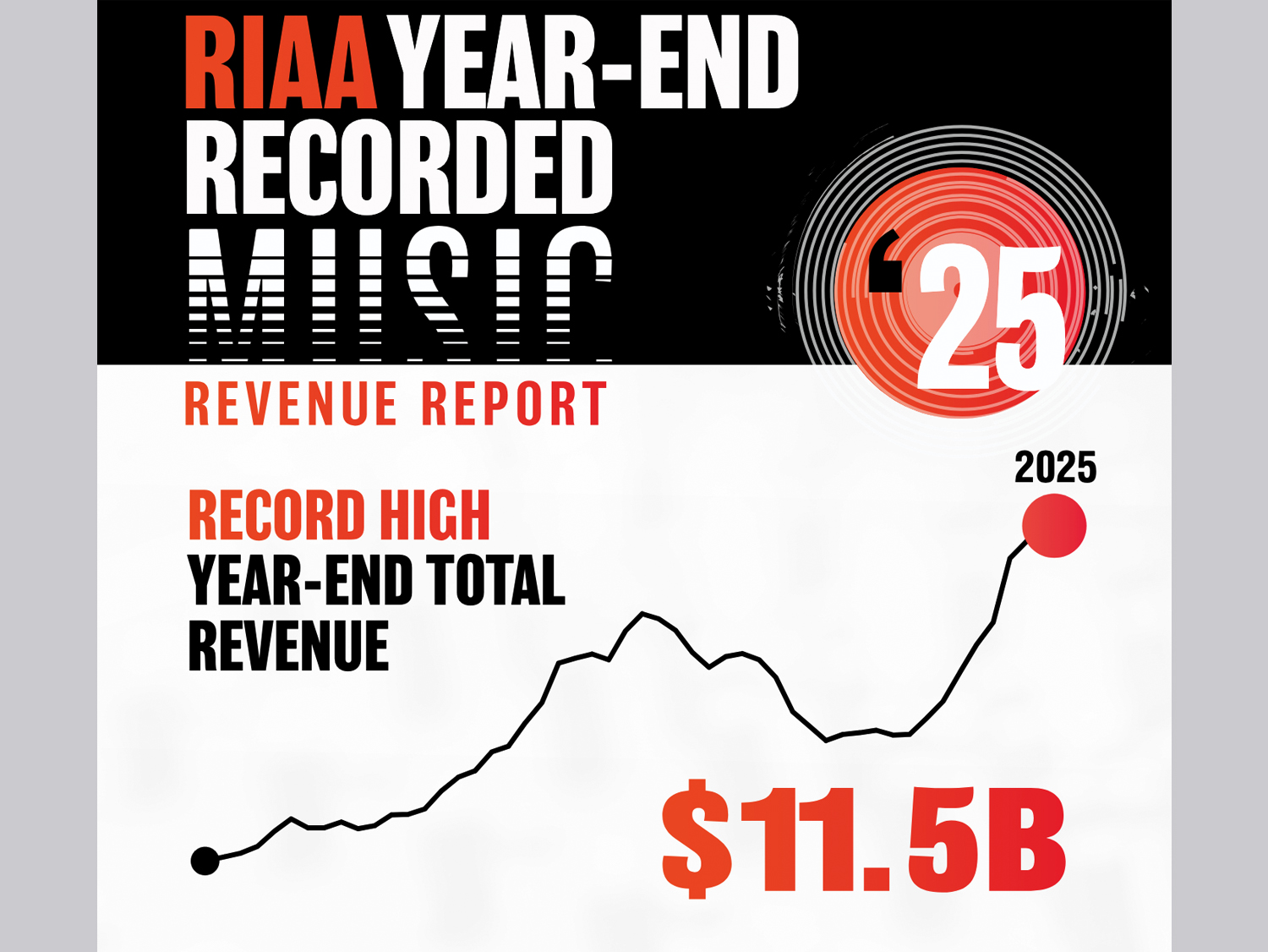

The US music industry just posted a number that would have seemed impossible a decade ago. According to the RIAA’s 2025 Year-End Report released in March 2026, total recorded music revenue in the United States climbed to $11.54 billion — a new all-time high and a 3.1% increase over 2024. But the real story isn’t the headline figure. It’s what’s driving it, what’s quietly resurging beneath it, and what it means for everyone who makes, distributes, or consumes music.

Streaming Still Runs the Show — But Growth Is Slowing

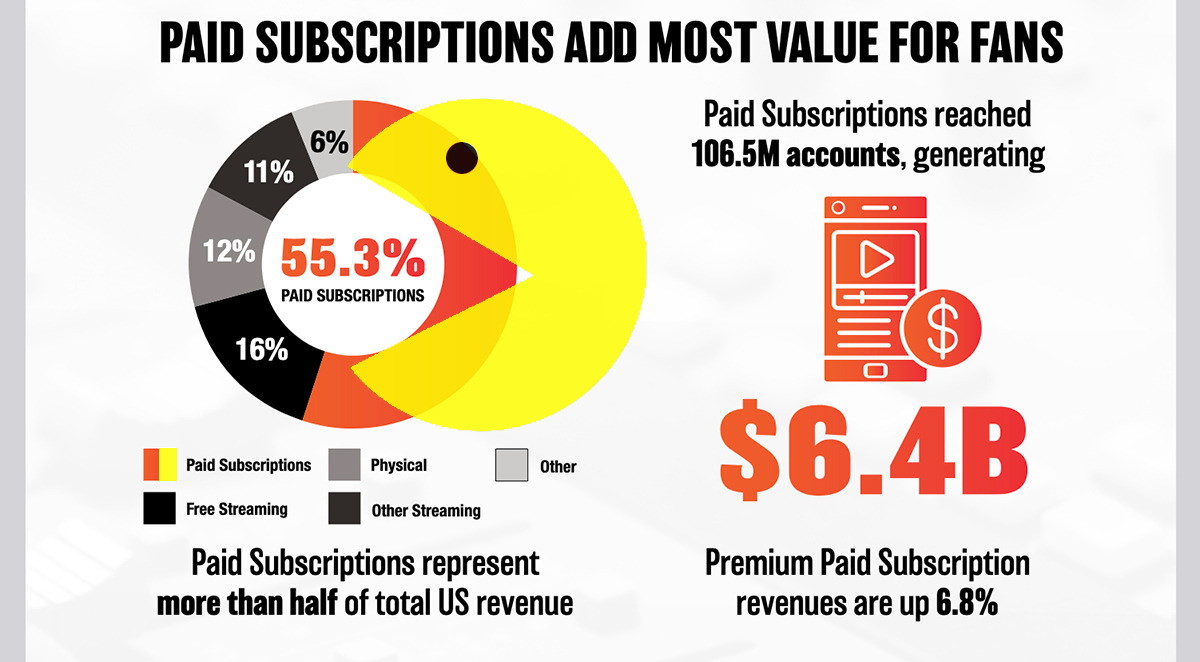

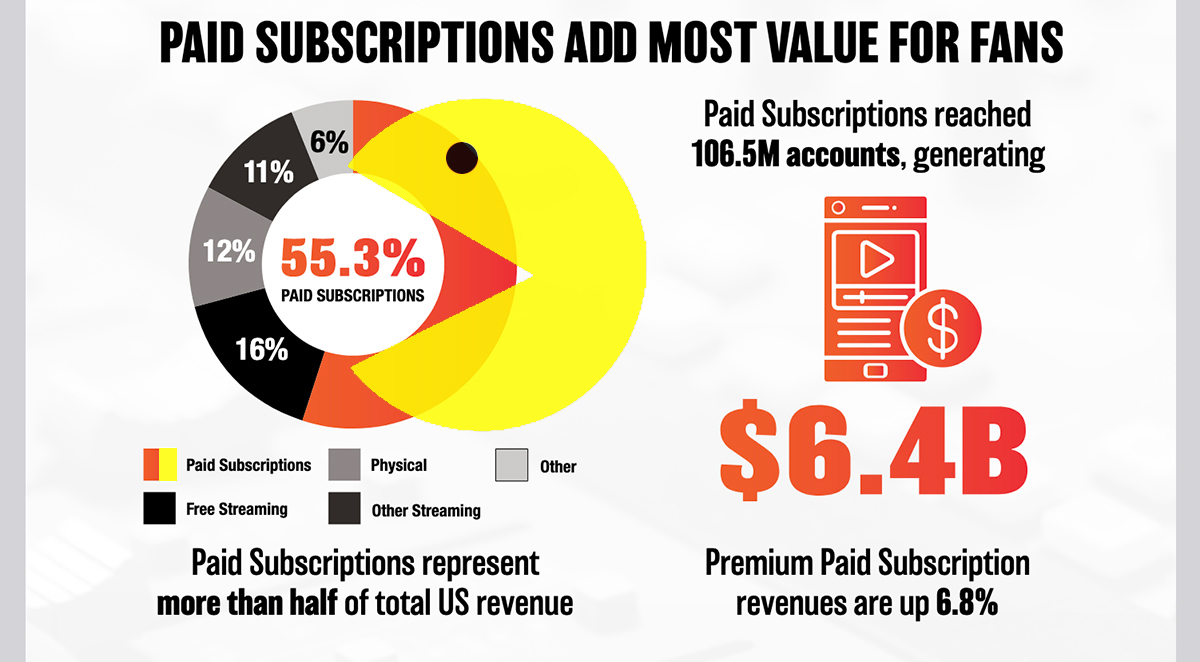

Streaming revenue reached $9.75 billion in 2025, up 3% from $9.46 billion the year before. That’s 84.8% of total US recorded music revenue — a dominance so complete that every other format combined barely registers as a rounding error in comparison. Paid subscription revenue specifically hit $6.38 billion, a 5.8% increase over 2024’s $6.03 billion, representing 55.3% of the entire market on its own.

The US now has 106.5 million paid streaming subscription accounts. That’s 6.5 million net new accounts added in 2025 alone — the strongest annual subscriber growth since 2022. For context, the US Census Bureau estimates roughly 131 million households in the country. We’re approaching a saturation point where nearly every household with broadband has a paid music subscription.

But here’s the nuance that matters: while subscriber counts grew at a healthy clip, total streaming revenue growth was only 3%. That gap between subscription growth (5.8%) and overall streaming growth (3%) tells us that ad-supported streaming revenue likely contracted or flatlined. The ad-supported model — which platforms like Spotify offer as a free tier — isn’t keeping pace. The industry’s revenue engine is increasingly dependent on people paying $10.99 or $11.99 per month, not on advertising dollars.

Vinyl Crosses $1 Billion for the First Time Since 1983

Perhaps the most culturally significant data point in the entire report: vinyl revenue surpassed $1 billion in the United States for the first time since 1983. Vinyl sales hit $1.04 billion on 46.8 million units sold, up 9.3% year-over-year from 43.4 million units in 2024. This marks the 19th consecutive year of vinyl growth — a streak that began when the format was essentially a curiosity item in 2007.

The US now accounts for nearly 50% of the global vinyl market’s value. That’s a staggering concentration. While vinyl represents less than 10% of total US recorded music revenue, its cultural significance and growth trajectory make it impossible to ignore. Consumers are voting with their wallets: they want physical ownership, album art they can hold, and the ritualistic experience of putting a needle on a record.

CDs, meanwhile, moved 29.5 million units. It’s a fraction of what they sold at their peak, but it’s notable that physical media collectively — vinyl plus CD — still represents a meaningful slice of the industry. The “death of physical media” narrative has been premature for about 15 years running.

The Revenue Concentration Problem Nobody Talks About

Here’s where the RIAA numbers deserve scrutiny rather than celebration. An $11.5 billion industry sounds enormous until you consider who captures that revenue. The three major labels — Universal Music Group, Sony Music Entertainment, and Warner Music Group — account for roughly 65-70% of recorded music revenue globally. Independent labels and artists split the remainder, often through distributors that take their own cut.

The per-stream payout economics remain challenging. Spotify’s average per-stream rate hovers around $0.003 to $0.005. An artist needs roughly 250,000 streams to earn $1,000 before their label or distributor takes a share. The 106.5 million subscribers are generating real money — $6.38 billion in subscription revenue — but the distribution of that money is heavily skewed toward the top 1% of artists and their affiliated labels.

This isn’t a flaw in the RIAA’s reporting. It’s a structural feature of the modern music economy that the headline revenue figure obscures. When we celebrate $11.5 billion, we should also ask: how is that money flowing, and to whom?

What This Means for Music Professionals in 2026

For producers and audio engineers, the RIAA data reinforces several strategic realities. First, streaming isn’t just dominant — it’s the only format that matters at scale for revenue. If your work isn’t optimized for streaming platforms (loudness normalization, metadata, playlist positioning), you’re leaving money on the table.

Second, the vinyl boom creates real opportunities for mastering engineers who understand the format’s unique requirements. Vinyl mastering is a specialized skill — managing bass frequencies for groove width, accounting for inner-groove distortion, and delivering a product that sounds great on turntables — and demand for that expertise is growing at nearly 10% annually.

Third, the subscription saturation trajectory suggests that future revenue growth will come from price increases rather than subscriber additions. Spotify, Apple Music, and YouTube Music have all raised prices in the past two years. Expect more. For artists and labels, this means per-stream payouts may actually improve over time as ARPU (Average Revenue Per User) increases, even if growth rates moderate.

The Bigger Picture: US Music in a Global Context

The RIAA report covers only the US market, but the US remains the single largest recorded music market globally, accounting for roughly one-third of worldwide revenue. The IFPI’s Global Music Report typically shows worldwide revenue around $30-32 billion, meaning the US alone generates more than a third of global music income.

What’s interesting is that growth rates in emerging markets — Latin America, Southeast Asia, Africa — significantly outpace the US. The 3.1% US growth rate is solid but mature. Markets like Brazil, India, and Nigeria are posting double-digit growth as smartphone penetration and affordable data plans bring millions of new listeners into the paid streaming ecosystem for the first time.

For the global music industry, this means the US will gradually represent a smaller share of total revenue — not because it’s shrinking, but because everyone else is growing faster. That’s healthy. A music economy that depends less on a single market is more resilient.

The RIAA’s 2025 Year-End Report paints a picture of an industry in good financial health but facing real questions about sustainability, equity, and the next phase of growth. Record revenue is worth celebrating. But the music professionals who thrive in 2026 and beyond will be the ones who read past the headline number and understand the structural forces shaping where the money actually goes.

Get weekly AI, music, and tech trends delivered to your inbox.

{kind=link}

{kind=link}

{kind=link}