Claude Year in Review: From 3.5 to 4.5 — How Anthropic Shipped 7 Models and Hit $1B in 12 Months

December 10, 2025

DeepSeek 2025 Year in Review: How a 200-Person Lab Wiped $600B and Rewrote the AI Playbook

December 11, 2025

The music industry just posted its strongest first half ever — and yet the biggest story might not be the record-breaking streaming numbers. It’s the 42-year-old format quietly sprinting toward a billion-dollar comeback, and the AI-powered disruptor threatening to rewrite the rules entirely.

Music Industry Revenue 2025: The Numbers That Matter

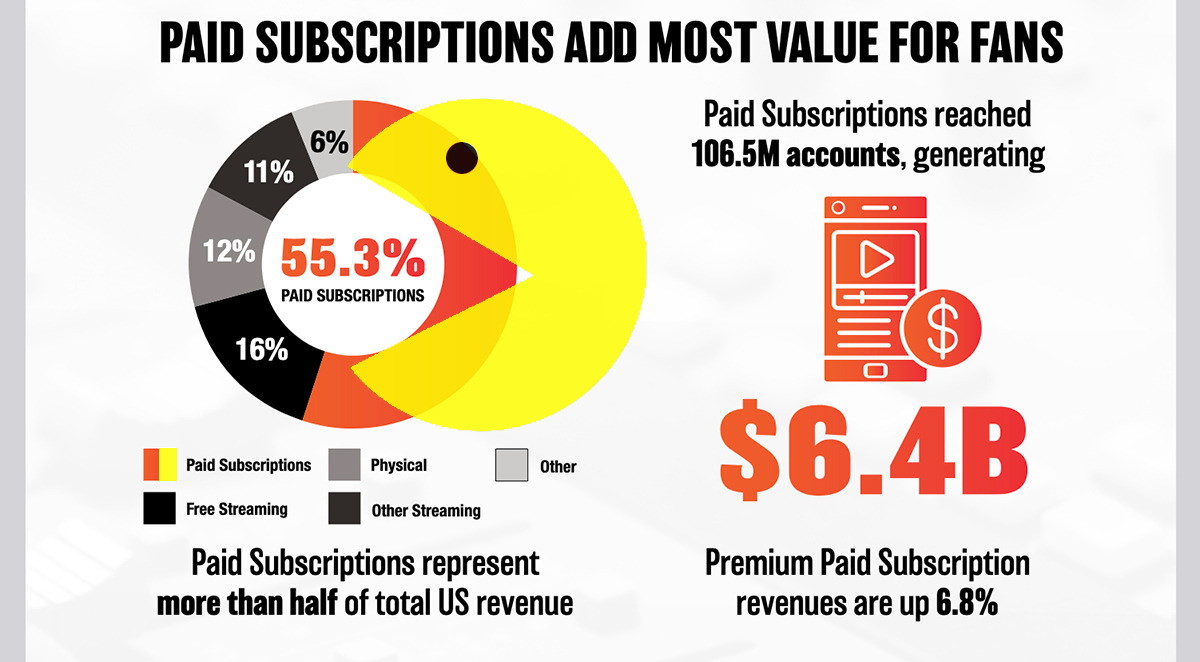

When the RIAA released its mid-year 2025 report in September, the headline figure was unmistakable: US recorded music revenue hit $5.6 billion in the first half of the year, setting a new all-time high on a wholesale basis. But look closer, and the growth rate tells a more nuanced story — less than 1% year-over-year improvement from 2024’s first half of $5.537 billion.

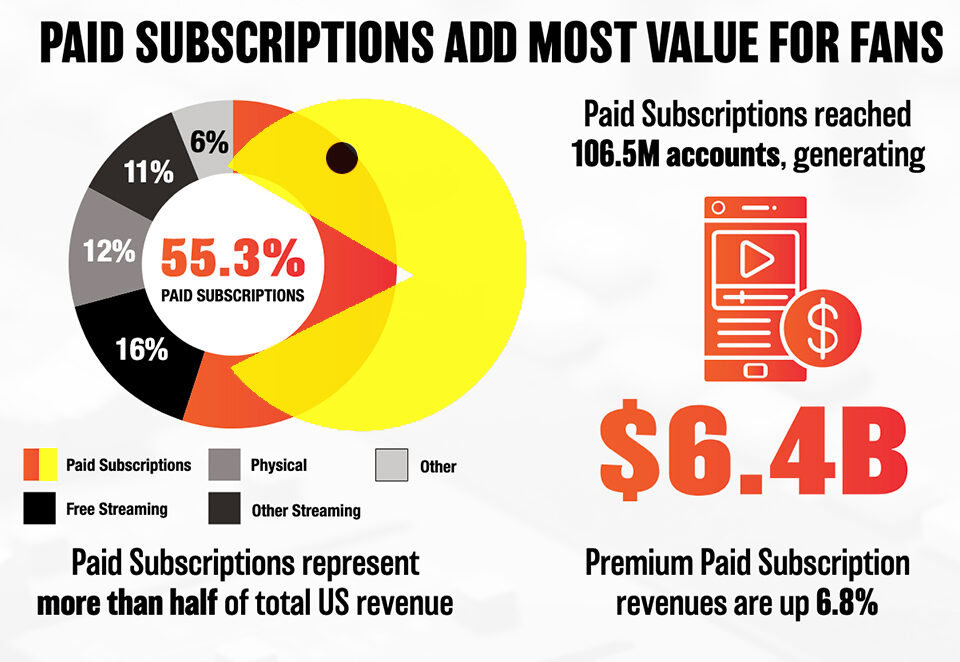

That deceleration matters. After years of double-digit streaming growth, the market is maturing. Paid subscription accounts crossed the 100-million threshold in the US for the first time, reaching 105 million — a 6.4% increase. Subscription revenue climbed 5.7% to $3.2 billion. These are still impressive numbers, but the days of explosive 15-20% annual jumps appear to be behind us.

It’s worth noting a significant methodological shift this year. Beginning with the 2025 reports, RIAA figures are reported on a wholesale basis rather than retail. This aligns with international benchmarks like IFPI’s Global Music Report and highlights the actual dollars flowing back into the creative ecosystem. The change makes year-over-year comparisons more complex, but the underlying trajectory is clear: streaming now accounts for 84% of total US recorded music revenue, with subscription services alone generating $3.2 billion in the first six months.

Synchronization revenue — music licensed for film, TV, advertising, and video games — deserves mention here as well. While not broken out in the mid-year headline, sync has quietly become one of the most lucrative per-track revenue sources for independent artists. Industry analysts estimate the global sync licensing market at over $1.5 billion annually, and it remains one of the few revenue categories where individual creators can earn substantial income without massive streaming numbers.

Global Picture: IFPI Reports 10th Consecutive Year of Growth

The global perspective, courtesy of the IFPI Global Music Report published earlier this year, paints a similar picture of steady but decelerating growth. Worldwide recorded music trade revenues reached $29.6 billion in 2024 — a 4.8% increase and the industry’s 10th consecutive year of expansion.

Streaming crossed a historic milestone, exceeding $20 billion in revenue for the first time ($20.4 billion), now representing 69% of all recorded music income globally. Paid subscription streaming grew 9.5%, with the global subscriber base expanding 10.6% to 752 million accounts. Latin America, Sub-Saharan Africa, and the Middle East emerged as the fastest-growing regions.

If current trends hold, the industry is on track to breach the $31 billion mark globally by year’s end — a figure that would have seemed inconceivable during the piracy-ravaged mid-2000s when annual revenues had dropped below $15 billion.

Streaming Market Share: Spotify, Apple Music, and the 90% Club

The streaming landscape remains remarkably concentrated. Spotify continues to dominate with 246 million premium subscribers globally (550 million monthly active users total), commanding a 36% share of the US market. Apple Music holds steady at approximately 30.7% domestically with around 94 million subscribers. Together with Amazon Music, these three platforms control over 90% of US streaming revenue.

Interestingly, Apple Music actually leads Spotify in US Family plan subscriptions by over four million accounts — suggesting that household-level adoption favors Apple’s ecosystem bundling strategy. As someone who has tracked these shifts for nearly three decades in the music business, this bundling trend is perhaps the most underreported story in streaming economics.

The streaming pie is growing, but the slices are largely spoken for. For newer entrants like Tidal, Deezer, and regional players, the path to meaningful market share has never been more challenging.

The per-stream economics remain a flashpoint. Spotify’s average per-stream payout hovers around $0.003-0.005, meaning an artist needs roughly 250,000 streams to earn $1,000. Apple Music pays slightly better at $0.007-0.01 per stream. These rates have been essentially flat despite rising subscription prices — the additional revenue has been absorbed by the growing catalog size rather than increasing per-stream payouts. For working musicians, this math increasingly favors diversified revenue strategies over streaming-only approaches.

Vinyl’s Remarkable Resurgence: On Track to Hit $1 Billion

Perhaps the most surprising storyline in music industry revenue 2025 is vinyl’s continued defiance of conventional wisdom. The format posted $457 million in US revenue during the first half alone, outselling CDs for the fifth consecutive year. If the second half follows historical seasonal patterns — and with holiday buying likely to provide a significant boost — vinyl is on pace to surpass $1 billion in annual US revenue for the first time since 1983.

That’s not a typo. The same format that the industry left for dead in the CD era is now generating more revenue than it did during its supposed golden age, at least in nominal terms. The average price of a new vinyl record has risen 24% since 2020 to $37.22, driven by premium pressings, limited editions, and collector demand. It’s now the 19th consecutive year of vinyl sales growth in the United States.

From a producer’s perspective, this matters enormously. Vinyl mastering requires specific considerations — different EQ curves, groove spacing, and dynamic range management compared to digital. Studios that invested in vinyl mastering capabilities five years ago are now seeing consistent demand, and that demand shows no signs of slowing.

AI’s Double-Edged Sword: Revenue Opportunity and Existential Threat

No analysis of music industry revenue 2025 would be complete without addressing the AI elephant in the room. The AI music market is projected to exceed $6 billion by year’s end, but the revenue story is complicated by the most significant copyright battles the industry has faced since Napster.

The RIAA’s landmark lawsuits against Suno and Udio — filed on behalf of Sony Music, UMG, and Warner Records — defined the year’s legal landscape. Both companies acknowledged training their models on copyrighted recordings while arguing fair use protections. The US Copyright Office weighed in with a May report questioning whether AI training on copyrighted works qualifies as fair use for music generation.

The tide turned in the fall. Udio reached a licensing agreement with UMG in October, followed by a WMG settlement weeks later. Suno and WMG announced their own settlement, with Suno committing to launch new “licensed models” while phasing out current ones. These deals suggest the industry is moving toward a licensing-based framework rather than outright prohibition — a pragmatic approach that could unlock significant new revenue streams.

But the fraud problem is real. Deezer’s internal data reveals that approximately 18% of content uploaded daily to the platform is AI-generated, and up to 70% of streams on fully AI-generated tracks are fraudulent. This streaming fraud directly dilutes the royalty pool that legitimate artists depend on.

What These Numbers Mean for Creators in 2026

As we close out 2025, three trends will shape music industry revenue heading into next year:

- Streaming growth is plateauing in mature markets. The US and Western Europe are approaching saturation. Future growth will come from emerging markets — Latin America, Africa, Southeast Asia — where per-subscriber revenue is significantly lower.

- Physical media isn’t dead — it’s premium. Vinyl’s march toward $1 billion proves there’s a substantial market for tangible music products. Artists and labels that invest in high-quality physical releases are capturing revenue that streaming alone cannot generate.

- AI licensing will become a new revenue category. The Suno and Udio settlements signal that AI companies will pay for training data. How that money flows to individual creators remains the critical unanswered question.

The music industry has recovered from its darkest decade and rebuilt itself into a $30 billion global business. But the nature of that recovery — dominated by three streaming platforms, challenged by AI disruption, and partially sustained by a vinyl format that refuses to die — would surprise anyone who predicted the future from 2010. The revenue numbers are strong. The question is whether they’re strong enough to support the millions of creators who make the music that drives them.

Want to stay ahead of the shifts reshaping the music and tech industries? Get weekly insights delivered straight to your inbox.

Get weekly AI, music, and tech trends delivered to your inbox.

{kind=link}

{kind=link}

{kind=link}